In the wake of 2010 banking regulations that require customers opt-in to get their overdrafts paid, and pay overdraft fees, banks have been pushing overdraft lines of credit as an “alternative to save you money.” Let's take a look at how good of a deal this really is for the typical bank customer.

What is an Overdraft Line of Credit?

An overdraft line of credit is essentially a credit card attached to your checking account. If you overdraw, the amount automatically is deducted from the credit account so you don't have a real overdraft on your account. An overdraft happens when your account balance goes below zero.

The new regulations are not working well, however, as banks made $32 billion from overdraft fees in 2012. Despite that increase, many banks still push customers into a “free” alternative to overdraft fees and offer the overdraft line of credit instead.

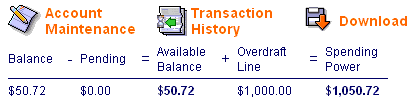

This image shows a snapshot of my Capital One 360 checking account (formerly ING Direct). At this point in time, I had a balance of $50.72 in my account and an unused overdraft line of $1,000. While I only had $50 in my account, the bank showed that I had $1,050.72 to spend including my overdraft line of credit.

Why Overdraft Lines of Credit Are Better Than Overdrafts

I am an advocate of this type of account, but only on several conditions.

- The line of credit should be free. If you have to pay to keep it active, monthly or annually, you are getting a bad deal.

- There should be no fee to use the line. If you are charged each time your bank makes an automatic transfer from your line of credit to your checking account, you may get a better deal just paying the overdraft fee. Depending on the bank, the overdraft line of credit access fee may still be less than an actual overdraft. In that case, it is your call which you prefer.

- Most importantly: You should be able to pay it all off at once any time from a linked savings account.

Like a credit card, most overdraft lines have interest attached. If you pay it off right away, you don't pay interest. It is more of a safety net.

I have an overdraft line of credit at Capital One 360, and it has been used once for about an hour. I had an auto-payment make a withdrawal on payday, though my paycheck had not processed yet. It was already used and paid off before I woke up! So it is a useful backup.

The Danger of an Overdraft Line of Credit

Never ever think of that line of credit as money you can spend. Like credit cards, it should be used as a backup and paid off immediately so you don't pay interest. I have never paid credit card interest and I have never paid overdraft line of credit interest. You should not either. Don't think of it as “spending power”, think of it as “what if”. In fact, don't even think about it. It is better to forget it is there and never dip below the zero in any of your accounts.

Do you have an overdraft line of credit? Have you ever used it? Share your stories on the comments.

Originally published October 29, 2008. Updated May 29, 2013. Image by Adam Bruderer / flickr.

I have an overdraft line of credit and the one time I actually used it saved me $25. I call that a win!

A nice win! Did they charge you anything to access the line of credit? Are there any monthly fees to keep it?

No monthly fees, but they charged me $10 for the one time use.

$10 is way better than $35! Do you do anything today to keep yourself from accidentally going over?

I just keep an extra $1,000 in my bank account at all times. That wasn’t an issue back then. 🙂

Great deal to read what you are doing now. Thanks for sharing your story.

I had one for a number of years, but then they wanted to start charging me for the service… now I’m just very careful not to overdraft.

That’s what I did with my old US Bank account, and then they wanted to charge me just to keep the account so I got rid of it completely.