Any long-time reader of Personal Profitability knows that I'm an investor in peer-to-peer lending at Lending Club. I write an occasional update on my portfolio, and compiled them all into a running history here. If you are interested in how I invest in Lending Club, check out my Ultimate Guide to Making Money with Lending Club.

Lending Club Update – April 16, 2009

After the first month of my trial at Lending Club, I am happy with the results. I have received my first payments ($1.66 per month) which I can track on the Lending Club site or on Mint. Here is my current outstanding loan break down.

As you can see, I have $48.85 left outstanding. Assuming I want to re-invest, I can do so in 14 months. At that point I will have recovered over $25 from my investments. Lending Club looks like it will take .01 per loan per month as a fee.

After my trial, I can confidently recommend the Lending Club product. However, each loan is different. As long as my borrowers keep paying, everything is good. It is up to them if I get paid back. There is no collateral, or protection for me, in case of non-payment.

I will keep you all updated as this trial continues. My $50 free is now growing by 12.21% per year, paid monthly. If you do sign up, be sure to look at each borrower closely. The letter grade system gives you a good idea of the risk you are taking on.

Lending Club Update – January 10, 2010

I have had some Peer to Peer lending excitement that I thought I would share. I have had both a scare and an early payment, but it seems that all is doing well in Eric's Lending Land.

First, I will share the scare and how it was resolved. I first noticed something was wrong one day when I logged in at LendingClub and saw that one of my loans was in the 31-120 day late bucket. The loan had a partial payment and missed payment. I was not sure if I would be out the $25 or if it would work out. This is the collection log as of today:

You can see where the trouble begins, on 11/6, with a failed payment. Since then, Lending Club worked diligently to bring the loan current. It took a few months, but things have smoothed out. I also got a $.09 late fee for my portion of the loan. (Click to enlarge)

I have also now had two loans payoff in full. That means I lose out on interest but get my entire outstanding principle back early. I can re-loan the outstanding principle into a new loan, and plan to do so shortly. My account balance today, including the outstanding loan, is $53.92. That is roughly a 7% annual return. Not bad at all.

Lending Club Update – September 3, 2010

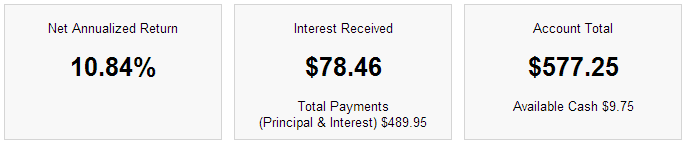

I have not written about Lending Club for a while, so I thought I would give you all the 4-1-1 on my investment.

You read that graphic correctly. My personal net annualized return is sitting north of 10.5%. While that is not huge in dollar terms, my growing loan portfolio now has five loans, all paid to date. My cash flow from the loan payments is about $3.90 per month. That is enough to invest in a new loan every six and a half months.

Lending Club started as an experiment using free money for signing up. It has turned out to be a great investment resource and I highly recommend anyone give it a shot. After all, why should the banks make all the money?

On average, Lending Club investors beat the S&P and Morningstar Bond funds by a substantial margin.

Lending Club Update – April 7, 2011

I have not written about my Lending Club experience in a while, so it seemed like a good time to share my progress. I have a net annualized return of 10.12%. When banks are paying below 1% interest, this is a great way to invest your money.

I am currently invested in seven different loans, each with a unique risk and return profile. I invested in three notes that have been paid off in full. As my account grows, I continue to reinvest in new loans. I started the Lending Club experiment with that philosophy.

At one point, I did have one loan over 30 days past due. If a loan defaults, you are out your investment. Fortunately the borrower has paid back all past due amounts and a late fee, which I get my portion of as well.

Lending Club Update – October 6, 2011

I have not written about my Lending Club experiment in a while, and hearing their name regularly at the Financial Blogger’s Conference over the weekend inspired me to give you all an update.

In my time with Lending Club so far, I have made 19 investments in $25 increments. Of those, four have been completely paid off, fourteen are outstanding and current, and one is in the funding process. None have defaulted, though I did have one scare that has since come current.

The more I use Lending Club, the more I appreciate what peer to peer lending has to offer. My average annual return has been 9.89%. I seriously suggest you check it out. I would not put all of my eggs in one basket and I would work hard to find diverse lending opportunities, but I would not overlook this blooming industry.

As a bonus, each reader who signs up for Lending Club investing through this link is directly supporting my efforts to keep going at Personal Profitability. If you want to understand how you can get such a high return, check out my old post on how you can make money like a bank.

As always, you can contact me in the comment page or comments below if you have any questions. If you are already on Lending Club, how has your experience been so far? Please share in the comments.

Lending Club Update – May 11, 2012

I began my Lending Club experiment in March, 2009 with $50 to see how I would fare in the peer-to-peer lending world. I have been thrilled with the results and have continued to slowly build my account.

As of now, I am earning a net annualized return of 10.10%. With savings accounts below 1%, this has turned into a great way to earn a better return, though there is also more risk.

I have made $46.63 in interest since I started with Lending Club, which is a great return given the size of my portfolio. I have invested in 24 notes in $25 increments and six of them have been fully repaid. One did go past due, but it was paid back into good standing by the borrower.

I have 17 outstanding notes with an outstanding principle of $301.43, one note in funding at $25, and $17.38 in cash. Every time my cash goes over $25, I pick a new loan right away.

Ever since I came up with the social lending snowball strategy, I have been considering adding $25 per month to my account to grow it even faster. I have not, as of yet, implemented the strategy, but it is in my long term plans for my investment strategy.

My biggest request of Lending Club would be to have an ability to do a direct deposit from my paycheck or an ACH from my checking account. At this point, you have to initiate the transfer from your Lending Club account, you can’t push money there from another source.

Overall, I have been thrilled with Lending Club so far and plan to grow that account while also giving Prosper a try. If you have tried peer-to-peer lending, I would love to hear about your experiences in the comments.

Lending Club Update – February 15, 2013

It has been a long while since my last Lending Club update. I am happy to share only good news as my social lending experiment moves forward.

Last year, I decided to build my Lending Club portfolio faster by automatically depositing $25 from each paycheck. My portfolio has certainly grown and I now have enough loans to add a new one each month from my lender payments.

Here is my current portfolio summary:

Loan Summary

I have made 39 loans so far, and 9 have been fully paid or paid early. I have 30 loans outstanding and all are issued and current. No loans are currently late and none have defaulted.

What excites me most about Lending Club are my consistent positive returns. One bad loan would be devastating to a portfolio this small, which is why I am trying to build it faster with 26 monthly deposits. I call this the social lending snowball.

Lending Strategy

From my time working in a bank, I know the biggest risk factors on a credit report. I review each loan I make individually and only choose the best loans. I am a stickler for low revolving debt balances, low revolving debt percent used, and late payment history.

Based on my strict guidelines, I am able to choose loans that are lower risk and better investments. Over time, I have relaxed my guidelines a bit to bring in higher-interest loans. Right now, I have 4 A-grade loans, 11 B-grade loans, and 15 C-grade loans. Over time, I will likely gravitate more toward C-grade and D-grade loans as my portfolio grows.

Making Social Lending Work for You

The key to doing well with lower grade loans is to have a lot of them. Just like banks spread around risk by building a big portfolio, as social lenders it is important for us to as well.

I don’t advocate making social lending the bulk of your investments, but I do suggest readers follow my lead and give it a try. If you deposit $500 to start, you can make 20 loans to distribute your risk. If you can’t afford that, you can start like I did with as little as $25 or $50.

Unlike stocks and mutual funds, you can’t quickly and easily sell your loans and walk away with the cash, so you have to treat these loans more like a CD with a cash flow. Your money is locked in until the loans are paid back. (There is a system to buy-sell on a secondary market, but it is not as easy as selling a stock.)

Give it a Try

If you have read about social lending before and never tried it, what are you waiting for? It doesn’t take a lot to get started, but the long term benefits are big. I have accounts at both Lending Club and Prosper and recommend either site. Full disclosure: I have most of my loans at Lending Club.

Lending Club Updates Going Forward

Thanks for reading my history of Lending Club updates! Going forward, I'm going to give you an update in my monthly net worth and income reports. Check in there for a monthly chronicle of my Lending Club loans. (Note, I ended adding Lending Club updates monthly in 2016)