Owning a home is still a large part of the American Dream. While that dream has shifted in recent years with the housing bubble, it is still a goal for many and an investment that can pay off in the long-term.

But finding the perfect home at the right price is only one aspect of the home buying process. Another major part of the process — where to obtain financing for the home — if not done properly can be costly.

According to results of the National Survey of Mortgage Borrowers, home buyers are ill-informed when it comes to mortgages and interest rates. Relying on their lender, broker or real estate agent, few borrowers search out or seek information from outside sources; almost half consider only one lender when submitting a mortgage application or place a greater priority on other factors such as maintaining a relationship with an existing financial institution instead of the overall cost of the loan.

These findings are interesting because it indicates that consumers aren't doing all the necessary research in order to find the best rate and mortgage available.

If you are thinking of buying a home, here are three simple steps you can take to find the best mortgage.

Educate Yourself About Mortgages

Even before you start searching for your home, take the time to educate yourself on the basics of mortgages. Why is this crucial? Educating yourself in advance can help you determine:

- How much home you can afford

- What type of mortgage features and terms are available and which may best fit your needs

- Special programs (such as first time buyer assistance) that may be available

- Income and down payment requirements

- Credit and FICO score requirements

The Consumer Financial Protection Bureau website provides a wealth of information to assist you in understanding the basics of home loans.

Being an informed consumer can help you ask the right questions as you search for and apply for a mortgage; help you evaluate the tradeoffs between a lower interest rate and higher upfront fees and help you find a lender who can offer a mortgage that fits your needs and budget.

Do Your Research

Once you’ve become familiar with the various types of home loans available and determined how much home you can afford, your next step is to search for potential mortgage lenders. In the age of the internet, you can find a substantial amount of information about your prospective lender online. Start by comparing reviews of various mortgage companies to see what might be a good fit for your needs. After completing your research, make a list of five viable lenders.

Shop Around

When looking for a mortgage, financing terms and interest rates vary among lenders. Despite this variance among lenders, nearly 50% of mortgage loan applicants fail to shop and compare rates.

Because you’ll be borrowing hundreds of thousands of dollars, selecting the mortgage that best meets your financial needs is critical. Selecting a mortgage haphazardly can significantly impact your finances over the long term. Even a small difference of .5% in interest can add up to significant savings (or cost).

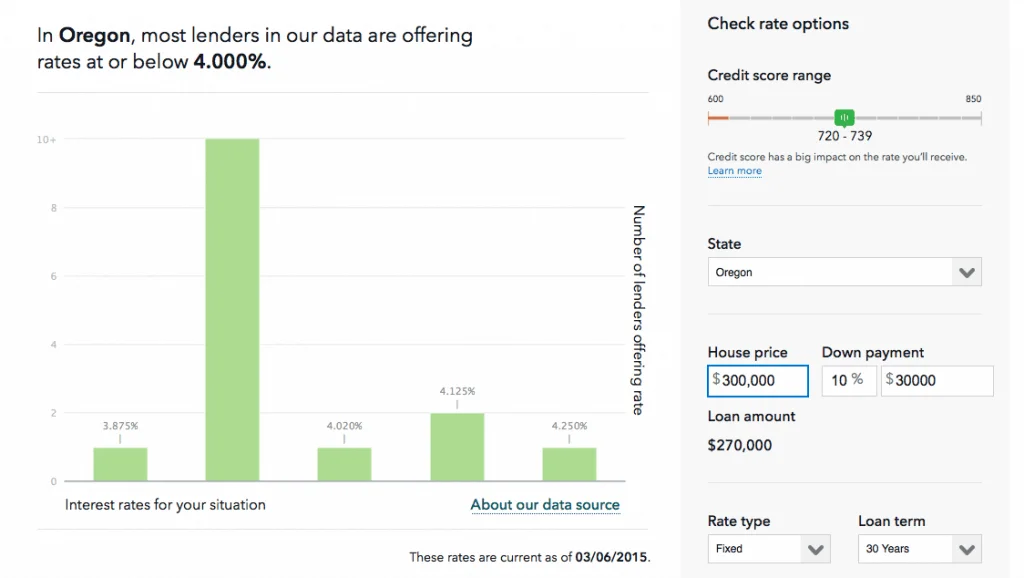

In order to get the best rate possible, it's crucially important that you shop around and compare various lenders. To assist in making these comparisons, you can utilize a nifty new tool designed for prospective home buyers. In an effort to help consumers make smarter decisions about mortgages, The Consumer Financial Protection Bureau recently released a new tool to assist in finding the best interest rates available. By simply entering your credit score, state, down payment amount, house price, and loan amount you can see how much more in interest you will pay over time, when you compare various interest rates.

As consumers we regularly research and compare features, options and costs before we buy an automobile; select a mobile phone carrier or buy electronics. However, when it comes to home buying, we often neglect to research options which can have significant financial implications.

Buying a home is one of the biggest and most important financial decisions you’ll make in your lifetime. Take the time to educate yourself on your options; identify a pool of potential lenders and compare rates and features to ensure you’re getting the best possible deal.

I’m finally getting a credit card at age 25 so I can get a low mortgage rate when I buy a home within the next 5 years. My credit score is 708. Hopefully I can have it in the 800’s by the time I’m 30. Gotta save even .5%!

Nice! Yeah, that can add up!

708 is a good score, and around where I was at 25. I just broke 800 within a month or so of my 30th birthday.

There is no real benefit of an 800 score vs a 760 credit score, other than #FinConpickuplines.

Haha about the FinCon comment.

You are now my role model. 800 (or at least 760) by 30 here I come!

My peak score was 822 (VantageScore 3.0) in December before our new mortgage hit my credit report, a full two months before I turned 30! ha ha.

Now I’m sitting at a cool 802 at TransUnion and 810 at Equifax.