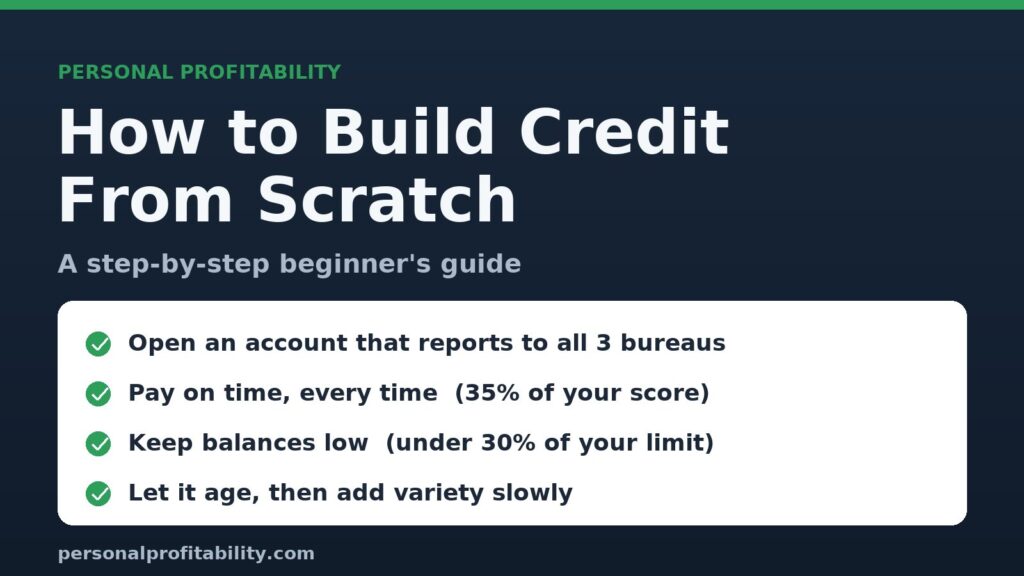

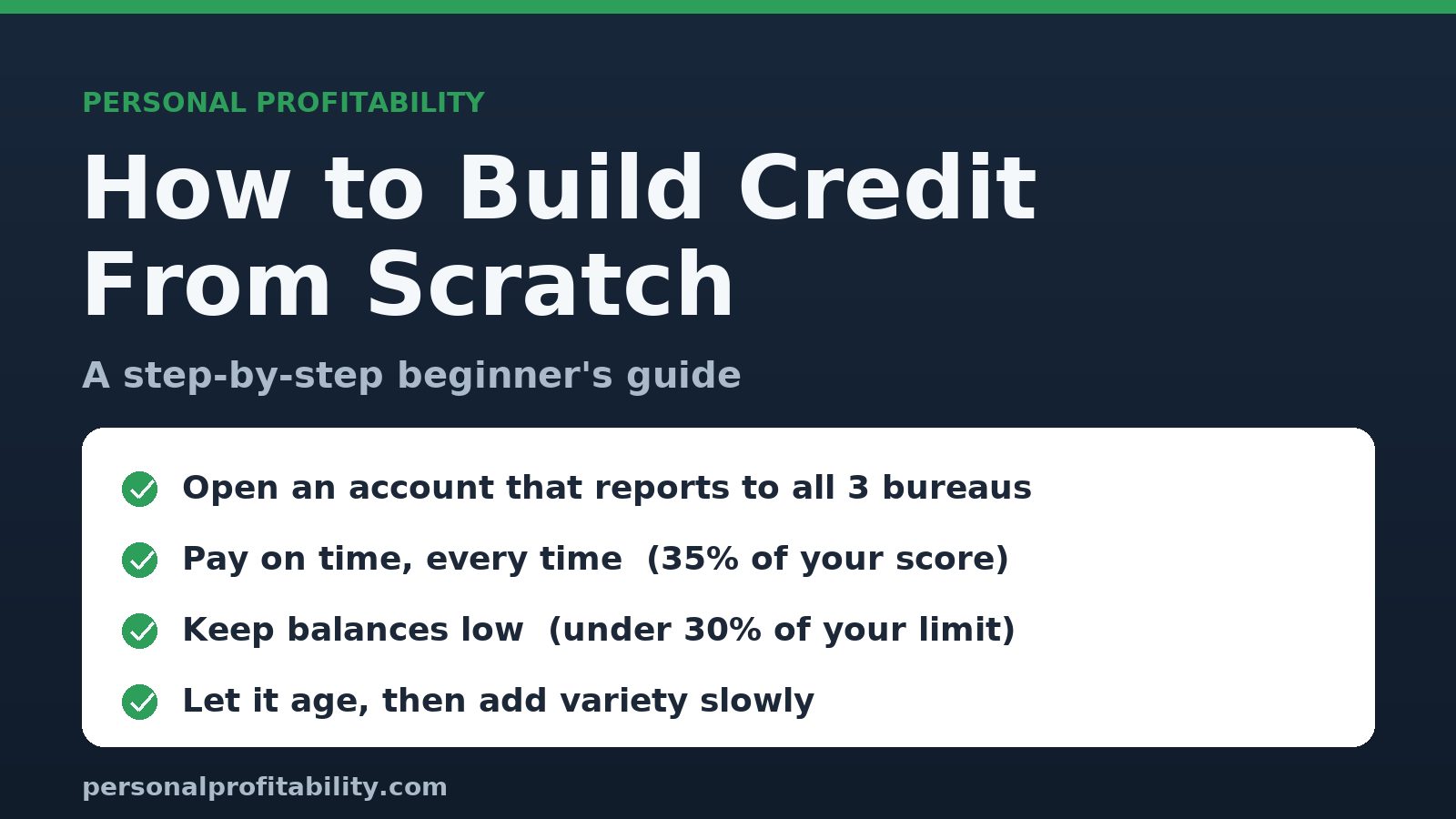

Here's how to build credit from scratch. Open a starter account that reports to all three credit bureaus, like a secured credit card or a credit-builder loan, pay every bill on time, and keep your balances low. Do that for about six months and an empty file turns into a real credit score.

Never borrowed money? Then you're not bad with credit. You're invisible to it. Lenders, landlords, and some employers can't see a track record, so a blank file reads as a risk, and they charge you more or say no. The fix is a short, clear process you can start this week. This guide from Personal Profitability walks through the exact steps, the accounts that actually report to the bureaus, the numbers that move your score, and the mistakes that keep beginners stuck. That's all there is to how to build credit from scratch, and it's more doable than it sounds.

What “no credit” really means

No credit isn't the same as bad credit. A thin or empty file gives the scoring models nothing to read, so they can't rate you at all. Millions of U.S. adults are “credit invisible,” a group the Consumer Financial Protection Bureau has tracked for years, and most of them simply never opened the kind of account that reports to a bureau.

That gap costs more than it looks. A blank file can mean a higher interest rate, a bigger security deposit on an apartment, a denied card application, or a utility company that wants cash up front. Build a short, clean history and those doors open. You don't have to be rich or carry debt. What you need is a few accounts that report to the three nationwide credit bureaus, Equifax, Experian, and TransUnion. Good credit lowers your interest rates, helps you qualify for better cards, and makes renting an apartment easier, so the payoff is real.

What goes into your credit score

Your FICO score comes from five things, and two of them carry most of the weight. Payment history (35%) and how much of your limit you use (30%) make up about two-thirds of the score, per FICO. For a beginner, that's good news, because both sit fully in your control from day one. That's why how to build credit from scratch is less about money and more about habits.

| Factor | Weight | What it measures |

|---|---|---|

| Payment history | 35% | Whether you pay on time, every time |

| Amounts owed (utilization) | 30% | How much of your available credit you're using |

| Length of credit history | 15% | How long your accounts have been open |

| Credit mix | 10% | The variety of accounts (cards, loans) |

| New credit | 10% | How many new accounts you've opened recently |

Want the longer version of how this works? Read our primer on what a credit score is and why your credit score matters. The short version is simple. Pay on time and don't max out your limits, and you're already nailing the two biggest factors.

How long does it take to build credit from scratch?

Plan on about six months to get your first FICO score. To generate one, your file needs at least one account that's been open for six months or more, plus at least one account reported to a bureau within the past six months, according to FICO. A single account can satisfy both rules.

So the clock starts the day you open that first reporting account, not the day you decide to fix this. VantageScore, the other main model, can sometimes produce a score a little sooner. Either way, a score shows up fast. A strong score takes longer, usually a year or two of steady, on-time payments and low balances. Open your first account now and your future self gets the head start.

7 steps to build credit from scratch

Below are the seven steps in how to build credit from scratch, in order. Not all of them happen at once. Begin with step two or three, then layer the rest in over the first year.

- Check your credit reports first. Pull all three for free, weekly, at AnnualCreditReport.com, the only federally authorized site. Confirm you really have no file, and catch any errors or signs that someone opened an account in your name.

- Open a secured credit card. You put down a cash deposit, often $200 to $500, and that deposit becomes your limit, the CFPB explains. Use it for one small recurring bill, pay it off in full each month, and pick a card that reports to all three bureaus and refunds the deposit once you graduate.

- Or get a credit-builder loan. A bank or credit union holds the loan amount in a locked savings account while you make small monthly payments for 6 to 24 months. When you finish, the cash is yours. You build a payment record and a little savings at the same time, with no debt along the way.

- Become an authorized user. Ask a parent or partner with a long, clean card to add you as an authorized user. Their good history can flow onto your file. The CFPB's research found that authorized-user-only files are weaker on their own, so treat this as a boost, not your whole plan.

- Pay every bill on time, every time. Payment history is 35% of your score, the single biggest factor. Set autopay for at least the minimum on every account so one busy month never costs you a late mark. Consistent, on-time paying builds a positive payment history, and a single 30-day late payment can undo months of progress.

- Keep your balances low. Amounts owed is 30% of your score. A common guideline says to use less than 30% of your limit, and lower is better. On a $500 secured card, that means holding the balance under about $150, even though you pay it off in full.

- Let it age, then add variety slowly. Time does the rest. Leave your first account open, since length of history is 15%. After a year of on-time payments, a second account type (a card if you started with a loan, or the reverse) helps your credit mix without spooking the new-credit factor.

Secured card vs. credit-builder loan: which should you start with?

Reach for a secured card if you want flexibility and a path to a regular card. Choose a credit-builder loan if you'd rather not touch a card at all and want to bank some savings while you're at it. Both report to the bureaus, both build payment history, and running them at the same time is fine. Here's the side-by-side.

| Secured credit card | Credit-builder loan | |

|---|---|---|

| How it works | Cash deposit becomes your spending limit | Loan amount is locked in savings until you pay it off |

| Cash up front | Refundable deposit, often $200 to $500 | Little or none, you pay over time |

| What it builds | Revolving credit history | Installment credit history plus savings |

| Best for | People who want a card and will pay in full | People who'd rather not carry a card |

| Watch out for | High fees or APR on weak cards | Setup or monthly fees, missed payments still hurt |

Your own bank or credit union is the first place to ask for either one, since a relationship already exists there. Compare the deposit, the fees, and whether the account reports to all three bureaus before you sign up. Weighing a regular card for later? Our guide to how to choose a credit card walks through the trade-offs.

How to build credit faster (without gaming it)

You can speed this up with a few honest moves, none of which involve tricks or paid “credit repair.” The fastest path is still on-time payments and low balances. Knowing how to build credit from scratch is half the job, and these habits handle the other half.

- Pay before the statement closes. Card issuers report your balance once a month, usually on the statement date. Knock it down before that date and a lower balance gets reported, which keeps your credit utilization low.

- Ask for a limit increase after 6 to 12 months. A higher credit limit with the same spending drops your credit utilization automatically. Check whether it's a soft pull first.

- Look at a student credit card if you qualify. Students often qualify for starter credit cards built for thin files, an easy way to add a second account and build credit responsibly. Use it lightly and pay it off in full.

- Keep your oldest account open. Closing your first card shortens your credit history and can bump your credit utilization. Leave it open and use it lightly.

- Don't apply for everything at once. Several applications in a short window add hard inquiries and lower your average account age, which hurts most when your file is thin. Space them out.

- Avoid credit repair companies. They can't do anything you can't do yourself for free, and the CFPB warns about ones that charge up front or promise to erase accurate information.

Check your credit reports every few months and watch the score trend, not the daily number. For the habit side of this, see our take on watching your credit report from a young age.

The bottom line

How to build credit from scratch comes down to one move repeated: open an account that reports to the bureaus, then pay it on time and keep the balance low. A secured card or a credit-builder loan gets you a score in about six months, and a year of steady payments turns that into good credit lenders like, which helps you qualify for better rates. No debt, no gimmicks, and no paid service required. Patience and autopay do the heavy lifting.

Pull your free reports first, then open your first reporting account this week. From there, keep learning: dig into what a credit score is, why it matters, and how to choose a credit card once you're ready to graduate. More waits in our Credit section. This is general guidance, not advice for your exact situation, so confirm the details of any account before you sign up.