The 50/30/20 budget rule splits your after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. It's one of the most practical budgeting methods in personal finance, and it actually works in real life. You don't need a spreadsheet, a financial planner, or a subscription app. You need last month's bank statement and about 20 minutes to see exactly how your spending lines up. This guide breaks down how the 50/30/20 budget rule works, what goes in each category, and how to apply the method when your income changes month to month. If you're building a budget for the first time, start with the Complete Beginner Guide to Budgeting to see how this rule fits into the bigger picture.

What the 50/30/20 Budget Rule Is and Where It Came From

Senator Elizabeth Warren and her daughter Amelia Warren Tyagi popularized this budgeting method in their 2005 book All Your Worth. Warren was a Harvard Law professor and bankruptcy researcher, and the method came from years of studying why American households fail financially. Their core finding: most budget problems aren't spending problems. They're structural. Too much of the paycheck is locked into fixed expenses before anyone decides where the money goes.

The three-category split was designed to fix that. Fifty percent to needs keeps fixed monthly expenses from crowding out flexibility. Thirty percent to wants gives you a real life instead of a joyless budget that nobody follows. Twenty percent to savings is the floor needed to actually build financial security over years.

Everything is based on your after-tax take-home pay, not your gross salary. The method only works when you start with the right number. After taxes, after payroll deductions, the real take-home is the baseline. That after taxes figure is what you divide. For freelancers and side hustlers, calculating that number takes one extra step, covered below.

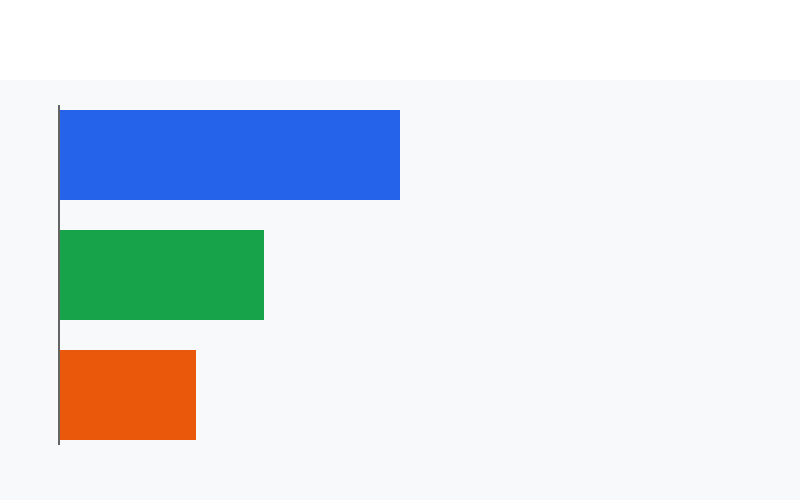

How to Calculate Your 50/30/20 Budget Numbers

Start with your monthly after-tax income and run three multiplications. That's the whole calculation. The method doesn't require categorizing every individual expense, just the totals across three broad buckets.

| Category | Percentage | Monthly on $4,000 | Monthly on $6,000 |

|---|---|---|---|

| Needs | 50% | $2,000 | $3,000 |

| Wants | 30% | $1,200 | $1,800 |

| Savings & extra debt | 20% | $800 | $1,200 |

Plug in your real monthly income after taxes and run the same percentages. Compare those three targets against your actual spending by category last month. The gap between what you spent and what the targets say tells you what to work on.

If housing expenses alone eat 45% of your take-home before you buy groceries, the method still tells you something useful: the exact size of the gap and what you'd need to earn or cut to close it. That clarity is the value. Most people have never run this calculation before, and the first time is usually revealing.

What Counts as a Need vs. a Want

This is where most people get the 50/30/20 rule wrong, and where honest categorization does the most work. A need is an expense you must pay to live and maintain your ability to work. A want is something you choose. The line is easier to draw than most budgets make it.

Needs include:

- Rent or mortgage payment (housing is the largest need for most households)

- Utilities: electricity, gas, water, and basic internet

- Groceries (the grocery store, not the restaurant)

- Transportation expenses: car payment, auto insurance, gas, or a transit pass

- Minimum required debt payments on student loans, credit cards, or any other loan

- Health insurance premiums

- Childcare required for you to work

Wants include:

- Restaurants, takeout, and coffee shop orders

- Streaming subscriptions (Netflix, Spotify, Hulu, and others)

- Gym membership, unless medically necessary

- Clothing beyond necessary replacement

- Hobbies, gadgets, and entertainment spending

- Vacations and travel

- Upgraded versions of things you already have: a bigger apartment, a newer car, the faster internet plan when the slow one works fine

- Shopping trips that aren't replacing a worn-out necessity

That last category is where budgets go sideways. A two-bedroom apartment when a one-bedroom works is a want. A car payment on a newer model when your current car gets you to the job reliably is a want. The 50/30/20 method categorizes based on what you need to function, not what you've grown accustomed to. Without that honest distinction, the 50% ceiling on needs means nothing.

How to Put the 20% Savings Category to Work

The savings category is the one that changes your financial future. It covers two things: building assets and paying down debt faster than the minimum requires. The order you fund these goals matters.

- Emergency fund first. Keep 3 to 6 months of living expenses in a liquid savings account before you invest a dollar anywhere. One unexpected expense without a buffer means the savings category immediately turns into new debt. See Emergency Funds 101 for how to build and size yours.

- Employer 401(k) match. If your employer matches any part of your 401(k) contribution, put in enough to capture the full match first. A 50% or 100% match on your contributions is an immediate guaranteed return that no other investment can match.

- IRA contributions. After the match, fund a Roth or traditional IRA. For 2026, the IRS sets the annual contribution limit at $7,500 per person, or $8,600 if you are 50 or older, according to the IRS retirement contribution limits page. Whether Roth or traditional depends on your tax situation now versus in retirement.

- Extra debt payments. Credit card debt payments above 15% APR cost more than most safe investments will earn. After the tax-advantaged accounts, direct extra funds toward high-rate balances. Paying off debt is a guaranteed return equal to the interest rate.

- Taxable investing. After the emergency fund, the match, the IRA, and high-interest debt payments are covered, invest the remainder in a taxable brokerage account.

Most people start with just the emergency fund and the employer match, then layer in the rest as income grows. The order matters more than the amounts when you're starting out. For more on building the savings habit, see Saving Money: How to Create Savings Habits and Goals.

How to Apply the 50/30/20 Budget Rule on a Variable Income

Freelancers, side hustlers, and business owners hit a real problem with this budgeting method: the rule says “50% of your income,” but what is your income when it changes every month?

Use your average monthly take-home over the last 6 months as the budgeting baseline. Add up 6 months of net income and divide by 6. If your income swings a lot, lean toward the lower half of that range rather than the average. Budget conservatively. You can always redirect a surplus to savings, but you can't un-spend what's gone.

In a good month, the extra goes to savings goals or extra debt payments. In a slow month, draw from your cash buffer rather than reaching for a credit card. That buffer, part of your emergency fund, is what makes variable income livable. Without it, one slow month blows the whole budget and the entire method breaks down.

One extra step for the self-employed: your after-tax income for the 50/30/20 rule is what's left after setting aside money for income taxes and self-employment taxes. Not gross revenue. Not the gross deposit to your business account. If you're not yet making quarterly estimated payments to the IRS, our guide to quarterly estimated taxes covers how that works and when payments are due each year. Budget the split against the real post-tax, after taxes number, not the gross.

The 50/30/20 Method vs. Other Budgeting Methods

The 50/30/20 rule is one budgeting method among several. Knowing how it compares to the alternatives helps you decide whether it fits your situation or whether you need something more granular.

Zero-based budgeting assigns every dollar a job, so income minus expenses equals zero at the end of each month. Zero-based budgeting requires more work: you categorize every transaction and plan every spending category in advance. It's the right method if you want maximum control over your expenses or if your spending patterns vary a lot month to month. The tradeoff is time. Zero-based budgeting is thorough but demanding.

The 50/30/20 method trades granularity for simplicity. You track three categories, not 30. You don't need to pre-plan every purchase or count every expense by line item. If you're new to budgeting or find detailed tracking unsustainable, the 50/30/20 rule is the better starting point. You can always move to zero-based budgeting later if you want more control.

The envelope method uses physical or digital envelopes for each spending category. Like zero-based budgeting, it's highly structured. The 50/30/20 rule is simpler than the envelope method and more forgiving, which is why it's often the method people actually stick with.

The best budgeting method is the one you'll use consistently. For most people starting out, that's the 50/30/20 rule.

When to Adjust the Percentages

The rule is a benchmark, not a contract. There are situations where the standard split won't work, and adjusting it is smarter than abandoning the method.

High cost-of-living areas. In New York, San Francisco, or Seattle, housing expenses alone can take 40% to 50% of median income. The method still tells you something: exactly how far above the benchmark you are and what income level would help you get under 50%. In the short run, acknowledge the gap and work with what you have.

Entry-level income. At a starting salary, saving 20% might not be possible while covering necessary living expenses. Even 5% is a real start. The habit of always saving something compounds faster than the dollar amount suggests. Don't drop the savings category to zero because you can't hit 20% yet.

Aggressive debt payoff. In a focused push to eliminate a high-rate balance, temporarily redirect part of the wants category to savings and debt payments. A 50/10/40 split for several months can meaningfully accelerate payoff. That's a short-term posture, not a permanent change to the method.

Very high income. At some income levels, 30% to wants exceeds what you'd naturally spend. Let the surplus roll into savings or investments instead of inventing new wants to fill the bucket. The percentages are targets, not requirements.

Real 50/30/20 Budget Examples

The math is simple once you plug in real numbers. Here are two realistic budget examples using the 50/30/20 method so you can see exactly how to apply it to your own situation.

Example 1: $3,500 monthly take-home pay

Ask yourself: what's my real take-home after taxes? If it's $3,500, here's how the 50/30/20 budget strategy looks:

- Needs (50%): $1,750. Housing costs like rent or mortgage take the biggest share, typically $900 to $1,200. Add utilities ($150), groceries ($250), and transportation costs ($200 to $300) and you're at or near the budget limit. Minimum debt payments go here too.

- Wants (30%): $1,050. Dining, streaming, hobbies, and shopping. This is the category most people overspend. Track it for one month and the number will surprise you. A budget plan is the only thing that keeps it honest.

- Savings (20%): $700. Start by putting $400 into an emergency fund until it's fully funded, then redirect that $400 to a Roth IRA or extra debt payments. The steps are the same regardless of income: emergency fund, match, IRA, extra debt, taxable investments.

Example 2: $6,000 monthly take-home pay

At $6,000 a month after taxes, the 50/30/20 budget gives you real room to save money and still have a life:

- Needs (50%): $3,000. Higher income doesn't mean higher housing costs have to follow. If your specific rent and housing expenses fit under $3,000 with utilities and transportation, you're on budget. The 50/30/20 strategy rewards you for keeping fixed costs steady as income grows.

- Wants (30%): $1,800. More room to travel, dine out, and enjoy yourself without guilt. At this income level, the wants budget is usually enough to cover real quality of life. The goal is to spend to $1,800, not beyond it.

- Savings (20%): $1,200. At $1,200 a month, you can fully fund a Roth IRA ($625/month, $7,500/year), cover your employer match, and still have money left for extra debt payments or taxable investing. This is the income level where the plan starts to really compound.

The specific numbers change with your income. The strategy doesn't. Remember: the goal is to use the 50/30/20 rule as a starting point, not a straitjacket. Most people find that the 20% savings category is the hardest to protect in the first budget they write. Automate it first, spend what's left.

Frequently Asked Questions

Your First Step With the 50/30/20 Budget Rule

Pull up last month's bank and credit card statements. Add up what you actually spent in each of the three categories: needs, wants, and savings. Compare those totals against your take-home pay. That's your real budget picture, and the first time you run those numbers is usually the most useful 20 minutes in personal finance.

Most people find the wants category bigger than expected. Spending on dining, subscriptions, and shopping adds up quickly when nobody is tracking it. The savings category is almost always smaller. The 50/30/20 method makes both visible in one pass without requiring a category-by-category spreadsheet.

Once you see the gap, the next moves are clear. If needs are above 50%, housing or other fixed expenses cost too much or income needs to grow. If wants spending is above 30%, find the largest line items and cut them first. If savings are below 20%, set up an automatic transfer on payday so the money moves before you see it. Automated savings is the move that actually sticks because it doesn't depend on willpower.

For a complete walkthrough of building a budget from the ground up, see the Complete Beginner Guide to Budgeting. Once you're tracking the three categories consistently, see Saving Money: How to Create Savings Habits and Goals for practical ways to make the 20% automatic and put it to work over time.