Your credit score is one of the most important numbers you will ever have in your life. It is like your old GPA (grade point average) from school, except for your money. Banks, credit card companies, lenders, employers, and landlords can use your credit history to decide if you get a new account, loan, apartment, or even a job. At the same time, it can save you tens of thousands of dollars on a mortgage loan. Here is everything you need to build an excellent credit score, and how you can understand and use it.

Start with Your Free Credit Score

A lot of people think you can only get a free credit report, not a free credit score. WRONG! I have been using Credit Karma and Credit Sesame for years to get my credit score 100% free. You can try it out for free today too! It only takes a few minutes to get your score with free advice on improving it.

Benefits of a free credit score

The key benefits are clear:

See a complete picture of your overall financial health

Learn how the terms of your loans and credit cards compare to your peers and the market

Find personalized advice and see recommended products to help improve your credit

Once you have your free credit score, continue on and compare your score to the information below to map out a strategy to improve (or maintain) your credit score.

Credit Karma is my favorite credit score service (disclaimer: I write for them too).

In your day-to-day life, your credit score doesn’t matter much. It matters when you need to get new credit, like a loan or credit card.

Your credit score will help underwriters determine whether you are credit worthy for a new loan or line of credit. It will also impact your interest rate. Better scores help people qualify for the best interest rates available.

If you want a new mortgage loan, for example, your credit score may tell a bank that you don’t qualify at all. If you do, you may be able to save tens of thousands of dollars, or more, in interested depending on your score.

What is a Credit Score?

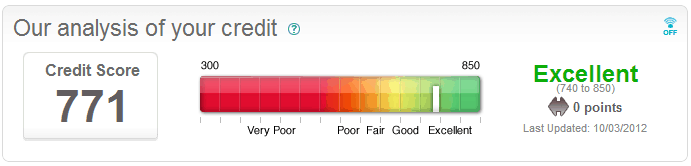

A credit score is a number between 300 and 850 that tells a lender if you have been responsible with past credit. An “excellent” score is generally a score that starts around 720-740 and above. Between 680-720 you are considered to have a “good” score. 620-680 is an “average” score. Below that, you have either a low, bad, or poor score and will have trouble getting new loans or credit.

The credit score is also called a FICO score, named for the Fair IssacCorporation, the company that developed the credit scoring system. Your score is generally reported by one of three credit bureaus, TransUnion, Equifax, or Experian.

In the long run, your credit score is a tool that you can use to accomplish your goals. Use your credit accounts to optimize your financial life. You don’t need an 850 credit score to get the best rates, you only need a score in the “excellent” category. Optimize your accounts to increase your score if you are in the market for any type of new credit or loan, such as a mortgage or car loan. Once you have those taken care of, it is okay if your score drops a little. I signed up for a new travel reward credit card, which lowered my score but helped me get free flights. That is worth it if you will not be getting any new loans in the near future.

What Goes Into My Credit Score?

Payment History – 35% of credit score

The single most important factor in your credit score is making on-time payments. If you pay any credit account late, the bank can report it to a credit agency. I wouldn’t suggest playing with fire, but most do not report a payment as late until 30 days.

After that, your account will certainly show your late payment. Being 30 days, 60 days, or 90+ days late on a credit or loan payment will have a big impact on your credit score. Be smart and pay on time.

Collections, public records, foreclosures, and bankruptcies impact this portion of your score calculation.

Outstanding Debt – 30% of credit score

We all have credit cards. (If you don’t, you really should have at least one.) We don’t all carry balances. How much debt is sitting on your credit cards, or any revolving debt, has the second biggest impact on your credit.

To calculate this portion of your credit score, the credit agencies calculate your credit utilization ratio. To calculate your ratio, add up the limit of all of your credit cards. If you have 3 cards with a limit of $5,000, $7,000, and $1,500, your total limit is $13,500. Next, add up your total balance on all of your revolving credit accounts (don’t include installment loans like a car loan, student loan, or mortgage). If you have balances of $500, $200, and $0 on those three accounts, your total balance in $700.

Last, divide your total balance by your total limit to calculate the utilization percentage. In this example, your credit utilization ratio would be 5%. The lower your number, the better your credit score. Over 20-25%, your score will suffer and you will have a tough time getting new credit.

Keeping a small balance to raise your score IS A MYTH. Having a utilization of 0% is the best way to keep a high credit score.

Length of Credit History – 15% of credit score

The average length of time your credit accounts is open makes up 15% of your score. Take the total number of months all accounts have been open and divide by the number of accounts to find your average. This calculation includes all accounts closed within the last seven years, so closing accounts quickly will lower your credit score.

My average age of credit is currently 3 years and 5 months. Having an average age of credit over 8 years is ideal, but difficult for young people.

New Credit – 10% of credit score

Applying for new credit gives you a “hard hit” on your credit report. Getting new credit both lowers your average age of credit and increases your new credit. That will lower your score.

If you are in the market for a new home or car loan in the near future, avoid all new credit to ensure your score does not suffer.

Credit Mix – 10% of credit score

When I got my mortgage loan in 2011, my credit score went up more than ten points! Why? Because I added a loan that indicates a stable and responsible borrower. If you only have credit cards, you are considered a riskier borrower than someone with installment loans as well.

Adding a car loan does not help you a whole lot, but adding a conforming mortgage can help bump up your score a lot. Of course, that doesn’t mean you should buy a house to help your credit, your credit should help when you decide to buy a house.

Where Credit Score Information Comes From: Your Credit Report

All of this data comes from your credit report. While the exact formula is a secret, you can look at your credit report (free from AnnualCreditReport.com).

Even if you don’t think you will ever need credit in the future, it is always a good idea to ensure your credit report is accurate and shows your ability to responsibly use and manage credit. Having a good credit score can save you a ton of money when applying for loans, and can save you having to put down a service deposit on phone or internet service. Most importantly, it can be used when you are applying for a job, and no credit history can raise as many questions and flags as a bad one.

What Information is in Your Credit Report

Your credit report is made up of all of the information around your current and past credit and loan accounts, with some age limits on older closed accounts. Every credit account you have open, and the entire payment history from those accounts, is included on your credit report. You can also find information on bankruptcies, collections, public records, and inquiries made over the last two years when you applied for new credit.

Some people believe that checking account overdrafts, your age, and your salary can be included in your credit report. None of those will ever be on your credit report, as your credit report only contains information related to credit accounts and indicators that demonstrate a positive or negative borrowing history.

How Can I Fix My Bad Credit Score?

YES! You can make your score better. To increase your score, I suggest closing all of your revolving credit accounts with negative information and keeping your accounts with a perfect history open. After seven years, the bad information will drop off and your good information will stay.

Don’t apply for lots of new credit if you want your score to go up. Patience and time will fix it. Also, make sure to dispute inaccurate negative information on your credit report. You can get a free credit report annually by law.

Short-Term Steps to Improve Your Credit Score

The first step in improving your long-term score is to make sure you are doing things right today. If you have a credit card balance, pay it off and always make payments on-time. If you have a loan, make at least the minimum payments every period. You should know if you have a problem in your history at this point from the steps above. If you do, it may take up to 7 years for negative information to drop from your report. That is why doing the right thing now is so important. If you are starting on your path to perfect credit for the first time today, you will be there in 7 years if you stick to it.

The number one thing you can do today to increase your credit score as quickly as possible is to pay off credit card balances to zero.

Remember that any “instant repair” offers you see are misleading. No one can do anything to fix your credit report and credit score other than you. It takes a long time to fix your credit, so make sure to start right away to get going on the right track.

Long-Term Steps to Improve Your Credit Score

Review Your Credit Report 3 Times a Year

You can get a free copy of your credit report from each of the major agencies once per year by law, but that doesn’t mean you should check them all at once. I spread them out so I can check my credit report every four months. You can get your free credit report from annualcreditreport.com.

Annual Credit Report is the only government mandated site to get your free credit report, any other site is trying to charge you for something you can get for free. Don’t waste your money on them.

Report Any Errors You Find

If you find inaccurate negative information, report it to the credit bureau and get it removed from your report. While you can’t remove accurate information, you should take the steps to move inaccurate information. I have done this before, and it was worth the time it took to fix my report.

To start the process, file a report with the credit bureau or contact the bank that reported the incorrect information on your report.

Eliminate Debt

While most of us don’t have enough cash on hand to pay off any outstanding debt right away, make a plan to pay it off over time. I used the debt snowball to pay for a car loan and school loans. I paid off my $90,000 education in 2 years. I am not that special, if I can do it, so can you.

Remove Negative Information and Keep Positive Accounts

Ultimately you want to keep all of the positive information and remove the negative information from your report. The next sections outline removing old information and keeping the good.

Negative Information Remains on Your Credit Report a Long Time

Negative information is anything ranging from a late payment to a bankruptcy. Regardless of what “credit repair” agencies tell you, they cannot legally help you remove any accurate negative information from your credit report. It is there as long as mandated by the credit reporting agencies, Experian, Equifax, and TransUnion.

Late payments – 7 years

Judgment – 7 years

Short Sale – 7 years

Foreclosure – 7 years

Tax Liens – 7 years from the final payment date

Chapter 13 Bankruptcy – 7 years

Chapter 7 Bankruptcy – 10 years

Improve Your Credit Utilization Ratio and Manage Your Credit Limits

Credit companies have become more cautious when issuing new credit, and some banks are even cutting credit for people with inactive accounts and increased credit risk. This can have important and costly ramifications on your credit, so it is important to understand how scores are calculated and what your credit limits mean.

What are Credit Limits?

Credit limits are one of the most basic parts of a revolving credit account. When you get a new credit card, the bank decides how risky you are and how much they would be willing to lend you. A college student with no credit history may be given a $500 limit while a homeowner with a long history may get a credit line over $100,000. My first credit card had a $700 limit. I have credit cards with limits well over $20,000 today.

How to Keep Cards Active

I once had a bank close one of my credit cards for inactivity. Having worked in a bank, I used to look at inactivity reports to decide which accounts should be shut down. It is really easy to avoid those reports.

To keep your account active, just use it every once in a while. I have around 10 open credit cards. I only use one every day. For the rest, I grab the stack a couple of times each year and buy lunch or gas or a small purchase on each card and pay it off right away. That keeps your account active, your limits high, and your ratio low.

How to Get Higher Limits

If you have a few cards with low limits, the easiest way to raise your total available credit is to ask. I have filled out the form at Citibank before and had an instant credit line increase of thousands of dollars. On an old MBNA card, I wanted a higher limit so I called and asked. They asked why I needed a higher limit so I told them I was planning a big trip and wanted to book everything on that card. They glanced at my payment history, which was flawless, and doubled my credit card limit on the spot.

New Credit Can Lower Your Score in the Short Term

One word of caution when seeking higher limits. New credit makes up 10% of your score. More new credit is considered a bad thing, so if you are planning on buying a home with a mortgage or seeking any new loan in the near future, hold off on getting new credit cards or submitting other applications.

How to Fix Errors on Your Credit Report

On occasion, banks report incorrect information on your credit report, which can dramatically lower your credit score and lower your ability to get a new loan at the best possible rate. I have found errors on my credit report in the past and took the steps to get them fixed.

The first step is to contact the financial institution that reported the incorrect information and try to work with them to make a correction. Corrections can take months to show up, so it is important to set calendar reminders and check on your report on occasion to verify that changes were made if the bank agrees to make the changes.

If you don’t have any luck there, contact the credit reporting bureau directly. Equifax, Experian, and TransUnion each have large dispute departments and can help expedite and mediate any incorrect information and work with you to verify that the information is incorrect and needs to be fixed.

This can be a frustrating process, but having a good credit score can save you tens of thousands of dollars on mortgages and other loans. A bad score can also keep you from the best credit cards, such as those with the best miles and points for travel hacking.

How Credit Cards Can Help (or Hurt) Your Credit Score

A credit score is not born overnight, over a month, or even over a year. It takes years to build a good score, and using a credit card responsibly can help you towards that end. On the other hand, poor credit card habits can cause your credit score to drop.

If you have a real spending problem, do not use credit cards. Not only will buying on credit lead to overspending and greater debt, but it can also negatively impact your credit score. On the other hand, if you have a good handle on spending and can pay off your balance every billing cycle, using credit cards can help boost your score. Plus, you get the bonus of reaping the rewards from your card issuer.

How Using Credits Cards Can Help

You create a consistent payment history: The most critical factor in your credit score is making on-time payments. If you have a credit card balance, at least pay off the minimum balance and always make payments on time. If you can pay off the entire balance each billing cycle, you should. You won’t pay any interest by paying off your card in full every month. If you only pay the minimum balance, you are paying up to 30% (or whatever the interest rate for your card is) to borrow that money.

You increase your average account age: As previously mentioned, the length of credit history accounts for 15% of your credit score. Keeping your credit card accounts open for a long time can increase your average account age, which is an easy way to establish a good credit score.

You maintain a low credit utilization ratio: Maxing out your credit cards is a big red flag for many credit companies, so only using a small percentage of your credit limit can help maintain your credit score (we’ll cover this in more detail later).

How Using Credit Cards Can Hurt

It’s not hard to spot the commercials and ads online from credit card companies showing all the ways that you can save money by making credit work for you, which is an ideal that has increased consumer dependency on credit. Consumers who responsibly apply credit for their purchases can raise their credit scores through timely payments. However, out-of-control debt and late credit card payments can negatively impact your credit score and future financial decisions.

A lot of times, credit cards can feed poor spending habits. In my time working in a bank, I had access to privileged information on people’s spending. I only looked at this information when the bank flagged people as “problem” customers. This happened when people were late on their credit cards or regularly overdrew their checking accounts.

What I found probably wouldn’t shock you. Most of these customers did not have income problems. They had spending problems.

Self-control is a real problem for many people, particularly young people, with credit cards. Using a $1,000 open credit line to buy a giant TV or a trip to Costa Rica can be tempting, but it is only a wise decision if you have the cash to pay that bill immediately.

Purchasing with a credit card instead of carrying cash can also make it harder to track spending, another reason credit card debt can quickly spiral out of control. And if you have a high credit utilization ratio or fail to make the minimum payment on your statement each billing cycle, your credit score could take a hit.

Your Credit Card Should Pay You

One of the biggest current misconceptions around credit cards is that they offer unique advantages, like travel rewards and cash-back offers. While some cards have worthwhile benefits, others have higher interest rates, and their rewards pale compared to savings in interest rates alone on another card. Paying money to make money simply doesn’t make sense.

Many people want to take advantage of travel miles and rewards, but there is a cost if you don’t pay the balance in full each month. Placing yourself deeper in debt to receive nominal benefits that accrue slowly may not be worth it in the long run.

Personally, I charge everything to my credit card. Everything. When I advise folks to stop using credit cards, I mean they should stop using the credit part, not the card. If you pay off your card in full every month, you pay no interest. If you don’t pay it all off, you are paying up to 30% (or whatever your interest rate is) to borrow that money.

So, I do charge everything. I pay it off in full twice a month (on payday). My balances are consistently low, so my credit score stays up. I pay in full, so I pay no interest. And, importantly, I get paid by the credit card company to use their card via cash back or travel rewards.

Is Closing a Credit Card a Good Idea?

People have lots of misconceptions about credit cards. Is opening more good for your credit score? Is closing a card good for your score? Do you want high limits or low limits? Do I need to use my card often to increase my score? Today, I’ll address one big misconception on whether or not it is a good idea to close a credit card.

Credit Utilization

30% of your credit score is determined by outstanding debts. The biggest factor in that part of your score is your credit utilization ratio.

Credit scoring companies think it’s bad if you max out your cards or use a super high percentage of available credit. Banks and lenders agree. To keep your score high, keep your balances low. 20% of available credit is a good reference point to use, though 0% is better!

For example, if you have a $10,000 limit on a card, you should always keep your balance under $2,000 to help keep your credit score high. But that 20% rule is not applied per account, it is across all revolving credit accounts.

If you have 3 accounts with a $3,333 limit (total of $10,000) and have a $2,000 combined balance, your ratio is 20%. If you close one but keep the $2,000 outstanding, your ratio just jumped to 30%, giving you a bad spot on your credit report.

Even if you never carry a balance, it can’t hurt having an extra cushion for unexpected situations

Average Age of Credit

The average age of open credit accounts and length of your credit history makes up 15% of your credit score.

Every time you open a new account, it lowers your average age of credit. If you have an account open for a long time, it raises your average age. If you have an old account and close it, your average age of credit stops increasing and that account will eventually stop being counted in the average.

To keep your credit score high, keep your accounts open as long as you can. I usually charge something small, like a $5-$10 lunch, on each card 1-2 times per year to ensure they are still “active accounts” and are not at risk to be shut down by the credit card company.

Annual Fees

BUT… There’s always a but.

As you read above, it is almost always best to keep your credit cards open, even if you don’t regularly use them. The big however is from annual fees.

If your card charges an annual fee, and you don’t use it, you are just throwing money away. Some cards are worth a fee if you are going to get a great benefit. I happily pay a fee on my Starwood American Express card because the benefits are so valuable.

If I did not get the value from the benefits, there would be no reason to keep the card open and keep paying for it.

Some banks will let you convert a card to one without an annual fee. That is the best option if you are able.

The Quest for an 850 Credit Score is Dead

When I started this site in 2008, I made it a goal to try to get a “perfect” credit score. Because the highest score possible is 850, I made that my goal. However, I realized over the years since that an 850 credit score could hurt me more than it could help me.

Logically, the goal in any pursuit is to be the best. Students try for 100% on tests. Athletes try for undefeated seasons. Bankers try for zero defaults. Consumers try for perfect credit scores. Hypothetically, a perfect credit score should not be difficult to attain. Keep your accounts open for a long time, never have a late payment, and you should be on the way. However, is it worth it?

750 vs. 850

There is a point that having a better credit score does not matter anymore. A credit score of 750 is considered “excellent” by most banks and lenders. At that score, you are going to qualify for the best possible interest rates.

So what is the difference if your credit score is 750 or 800 or 850? There isn’t really a difference. Unless you are a finance guru that needs to be able to prove how awesome you are or an asshole that brags about your credit score, it does not matter.

Why This Matters

I sign up for new credit cards all the time. Right now I have 15 of them. I am also planning to close a credit card with an annual fee. This will have two negative impacts on my credit score. It will shorten my average age of credit and possibly lower my available credit, giving me a higher used credit percentage.

However, my credit score will only fall by about 10 points. My score will still get me the best possible loan rates if I decide to get a new car loan or buy a new home.

Canceling the old card will save me a $95 annual fee and the new card will get me 50,000 bonus points with bonuses for transferring to miles from Chase Ultimate Rewards. This could be worth two round-trip flights in the US or one international round-trip flight.

Your Credit Score is a Moving Metric

Your credit score is always changing. New credit, aging credit, on-time payments, and new loans are common for people with good credit scores. If you always pay on time and manage your credit responsibly, you don’t have to worry about having credit that is not excellent.

Don’t worry too much about the extra points on your score. Do what you can to take advantage of great offers and discounts. Unless you screw up, your excellent credit isn’t going anywhere.

Take Control of Your Credit

I can’t tell you how many times I’ve come across someone blaming other people for their bad credit or personal finance situation. For us, that ends today. You control your credit cards and loans. Now you know how they work, so you are the only person in control of your credit report and credit score.

If you have not already, sign up for Credit Sesame to make sure you know what is happening on a regular basis. Check your AnnualCreditReport.com credit report at least once a year (I get the three reports spread out every four months). You have the tools and the knowledge to have excellent credit. Now it is time to make it happen.

This post was originally published on November 13, 2015 and last updated on October 11, 2023.

8 thoughts on “Credit Scores: The Complete Beginner Guide”

Jillian

AWESOME ADVICE – particularly about the no real difference between 750, 800 and 850. This is really important because I also have considered closing a credit card with a $95 annual fee and opening a new card to get 50,000 bonus miles. I am considering closing my Chase Sapphire Preferred card and opening a United MileagePlus card, moving my Chase Ultimate Rewards points to MileagePlus before closing the account. Are you considering the same thing?

Hi Jillian! You have a great thought process going on with your annual fee.

The Sapphire Preferred is one of the only cards with an annual fee that I consider a “keeper.” I am happy to pay the fee on that card for the huge benefits I get from it, including the ability to transfer miles to airlines instantly. I get well over $95 in value from the card, so it is one I am keeping indefinitely. If you do not get that same value, it is okay to close it down as far as your credit score is concerned.

If you are a regular United flyer, that is a great signup bonus. Moving your points to United before closing the Sapphire Preferred account is a must-do as well. You might consider having both cards – or just opening the United card for a year and then closing that one, but keeping the Sapphire Preferred – whatever best fits your needs.

If you do close the Sapphire card, I would open the United card first and ask Chase to move your open credit limit to the United card when closing the Sapphire card. Doing so will keep your total outstanding credit available high and your credit usage ratio low. Every time I close a card where I have another at the same bank, I ask them to move the open credit line over.

e.g. New United card has a $5,000 limit and Sapphire has a $10,000 limit. When closing the Sapphire, Chase can move the $10,000 (or most of it) to the United card giving it a total $15,000 limit.

Baron Kanter

Hey man, its been a long time! Your site is excellent and really provides great information. What are your thoughts on creditkarma.com? Their site seems very similar to quizzle.

Hey Baron! I have a CreditKarma account as well. I like the others a little better, but it is totally okay and safe to use. I know some (awesome) people who work there and stand behind it 100%. If the others did not exist, I would certainly use CreditKarma more.

Simon

When you say “the others”, what are you referring to? I love CreditKarma but I’m definitely open to alternatives 🙂

I was specifically referring to CreditSesame and Quizzle, though I am aware of some other options as well, in addition to the ability to get a score for free with some credit cards.

Mike A.

Eric, great article. Credit is something that cannot be trifled with and I am one to know. I had to rebuild my credit from sub-550 to 640 to buy my first house (good tip to know for Veterans–640 is the same as 850 in the VA’s eyes–same rate) with a VA loan. So at 640, I was able to get 3.25% for my house in San Diego.

To get from 550 to 640 I had to do a lot of leg work and it took about two years. After I got the first house, all it took was time to build my credit further. I now have a total credit limit of $150K plus ($50K in cash), with about 15 cards and am using about $2K.

About the FICO score. Both Discover IT card and my CitiCard give me my FICO score free on each statement. I also used CreditKarma in the beginning of my journey, but with these cards giving it free, I don’t check CreditKarma as much now.

When I bought our second house (keeping the first as a rental) I was able to get 4.1% (non-VA loan) but my credit was still under 720 at the time (but not by much–717).

Now, I am at 740+ regularly (changes monthly depending on what I do). Its been a journey. The best thing I can reinforce from your article is:

1) clean up your past

2) don’t ever be late

3) keep a very low utilization rate.

That is the core in my opinion. Opening and closing accounts after that are minor hits that don’t last long. That has been my experience.

About annual fees – I have one. My Delta AMEX Reserve. I got that because it bumps you ahead of other Delta Elite flyers on Delta for upgrades. I am 75% travel so if its between me and another Elite to get first class, I will get it with the card. Well worth it if you travel a lot like me.

Thanks for sharing your story Mike. It looks like you made great decisions to increase your score and buy the home you really wanted.

I’ve noticed a few of my credit cards giving me a free FICO score as well. I get one from Barclaycard, Citi, and American Express. It’s a nice perk since they have it anyway!

Stay in touch. I’m thrilled to have you here.

Comments are closed.

Manage your privacy

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

AWESOME ADVICE – particularly about the no real difference between 750, 800 and 850. This is really important because I also have considered closing a credit card with a $95 annual fee and opening a new card to get 50,000 bonus miles. I am considering closing my Chase Sapphire Preferred card and opening a United MileagePlus card, moving my Chase Ultimate Rewards points to MileagePlus before closing the account. Are you considering the same thing?

Hi Jillian! You have a great thought process going on with your annual fee.

The Sapphire Preferred is one of the only cards with an annual fee that I consider a “keeper.” I am happy to pay the fee on that card for the huge benefits I get from it, including the ability to transfer miles to airlines instantly. I get well over $95 in value from the card, so it is one I am keeping indefinitely. If you do not get that same value, it is okay to close it down as far as your credit score is concerned.

If you are a regular United flyer, that is a great signup bonus. Moving your points to United before closing the Sapphire Preferred account is a must-do as well. You might consider having both cards – or just opening the United card for a year and then closing that one, but keeping the Sapphire Preferred – whatever best fits your needs.

If you do close the Sapphire card, I would open the United card first and ask Chase to move your open credit limit to the United card when closing the Sapphire card. Doing so will keep your total outstanding credit available high and your credit usage ratio low. Every time I close a card where I have another at the same bank, I ask them to move the open credit line over.

e.g. New United card has a $5,000 limit and Sapphire has a $10,000 limit. When closing the Sapphire, Chase can move the $10,000 (or most of it) to the United card giving it a total $15,000 limit.

Hey man, its been a long time! Your site is excellent and really provides great information. What are your thoughts on creditkarma.com? Their site seems very similar to quizzle.

Hey Baron! I have a CreditKarma account as well. I like the others a little better, but it is totally okay and safe to use. I know some (awesome) people who work there and stand behind it 100%. If the others did not exist, I would certainly use CreditKarma more.

When you say “the others”, what are you referring to? I love CreditKarma but I’m definitely open to alternatives 🙂

I was specifically referring to CreditSesame and Quizzle, though I am aware of some other options as well, in addition to the ability to get a score for free with some credit cards.

Eric, great article. Credit is something that cannot be trifled with and I am one to know. I had to rebuild my credit from sub-550 to 640 to buy my first house (good tip to know for Veterans–640 is the same as 850 in the VA’s eyes–same rate) with a VA loan. So at 640, I was able to get 3.25% for my house in San Diego.

To get from 550 to 640 I had to do a lot of leg work and it took about two years. After I got the first house, all it took was time to build my credit further. I now have a total credit limit of $150K plus ($50K in cash), with about 15 cards and am using about $2K.

About the FICO score. Both Discover IT card and my CitiCard give me my FICO score free on each statement. I also used CreditKarma in the beginning of my journey, but with these cards giving it free, I don’t check CreditKarma as much now.

When I bought our second house (keeping the first as a rental) I was able to get 4.1% (non-VA loan) but my credit was still under 720 at the time (but not by much–717).

Now, I am at 740+ regularly (changes monthly depending on what I do). Its been a journey. The best thing I can reinforce from your article is:

1) clean up your past

2) don’t ever be late

3) keep a very low utilization rate.

That is the core in my opinion. Opening and closing accounts after that are minor hits that don’t last long. That has been my experience.

About annual fees – I have one. My Delta AMEX Reserve. I got that because it bumps you ahead of other Delta Elite flyers on Delta for upgrades. I am 75% travel so if its between me and another Elite to get first class, I will get it with the card. Well worth it if you travel a lot like me.

Thanks for sharing your story Mike. It looks like you made great decisions to increase your score and buy the home you really wanted.

I’ve noticed a few of my credit cards giving me a free FICO score as well. I get one from Barclaycard, Citi, and American Express. It’s a nice perk since they have it anyway!

Stay in touch. I’m thrilled to have you here.